How does “no tax on overtime” work?

Do I still withhold taxes for overtime hours?

How do I report overtime hours in 2026?

Do any of these questions sound familiar? If you, like many, are struggling to make sense of the new federal overtime tax exemption and what you need to do differently this year, then you’re in the right place. This article will help you understand the new overtime reporting guidelines, so your field crews get the tax breaks they’ve been promised, and you keep your company compliant (and audit-free).

New overtime tax at a glance

Here’s the TL;DR of the new overtime tax reporting:

Employees will receive overtime tax deductions, but only when filing their federal tax returns, not on paychecks.

Employers must follow new, more detailed overtime reporting requirements.

Inaccurate reporting could result in missed employee deductions and/or IRS penalties for employers.

New overtime tax rules for 2026

Signed into law in July 2025, the One Big Beautiful Bill Act (OBBBA) introduced a temporary federal income tax deduction for qualified overtime compensation (QOC) earned between 2025 and 2028.

The law was marketed under the slogan "No Tax on Overtime." However, this is a bit of a misnomer. The act allows eligible hourly workers to deduct the “premium” portion of their overtime pay from their federal taxable income, and defines that portion very specifically (see “What are qualified overtime hours?” below). That means your workers will receive the tax break as a deduction when they file their individual 2026 tax returns, not as an immediate boost to their paychecks.

Payroll implications: What does this mean for you?

As an employer, with holding has not changed. You must continue to withhold federal income and payroll taxes (Social Security, Medicare, etc.) from every paycheck. However, you are now also required to isolate and report QOC as a separate line item on every W-2, for which the IRS has officially designated Box 12, Code TT.

Starting with the 2026 tax year, the IRS has officially designated Box 12, Code TT, for reporting qualified overtime compensation.

Because the OBBBA was passed mid-year, the IRS provided a "transition relief" period, during which you were not required to use specific tax codes or even report overtime separately on 2025 W-2s. Instead, you could simply report "reasonable estimates" for the total number of OT hours worked. But not anymore.

As of January 1, 2026, that relief has expired. For the 2026 tax year, you are strictly required to track and report every dollar of qualified overtime. If you’re not prepared to track this level of detail in your payroll data, your accounting team will have to spend hours manually reconciling payroll at year-end, your employees may not get the proper tax deductions they’re owed, and if things are reported incorrectly, your company could be subject to IRS penalties.

What are "qualified" overtime hours?

The new legislation is very specific that the new tax deduction applies only to the premium portion of pay required by federal law (the extra “half” in time-and-a-half).

“In general, section 225 provides an income tax deduction for 'qualified overtime compensation', defined in section 225(c) as overtime compensation paid to an individual required under section 7 of the FLSA that is in excess of the regular rate at which the individual is employed.” – IRS.gov

For your accounting team, this means "total overtime" is no longer sufficient, and you must now be able to distinguish two specific components within your 2026 payroll data:

The "half-time" premium: You are only reporting the premium portion (the 0.5 in 1.5x) of the pay. The base hourly rate remains fully taxable to the employee (even on OT hours).

The FLSA threshold: The new tax deduction only applies to overtime required by the federal Fair Labor Standards Act (FLSA), which is typically any hours you pay over 40 in a single workweek. Overtime premium pay from union contracts or state/local laws does not qualify.

For overtime hours to be considered “qualified” for the tax deduction, both conditions must be met, and the FLSA overtime calculations have to be perfect. Unfortunately, this could mean hours of additional work for your payroll team.

Avoiding state and federal conflicts

Overseeing multi-state payroll always presents unique challenges, and, if we’re being honest, some contradictions with federal tax definitions. If you operate in a state like California, you would pay worker daily overtime after eight hours. However, if that worker doesn't cross the 40-hour federal weekly threshold, that daily OT is not qualified for the 2026 federal tax deduction.

The same applies to your union collective bargaining agreements (CBAs). While you may pay "double-time" for Sundays or holiday premiums, these are contractual agreements that generally exceed the federal reporting requirement. To illustrate what this difference looks like in practice, here’s an example from the IRS website:

“Brad’s employer has a practice of paying overtime at a rate of two times an employee’s regular rate of pay, and Brad was paid $20,000 in overtime pay during 2025. Brad’s last pay stub for 2025 shows “overtime” of $20,000 paid in 2025. For purposes of determining the amount of qualified overtime compensation received in tax year 2025, Brad may include $5,000 ($20,000 divided by 4).”

How to calculate qualified overtime premium pay

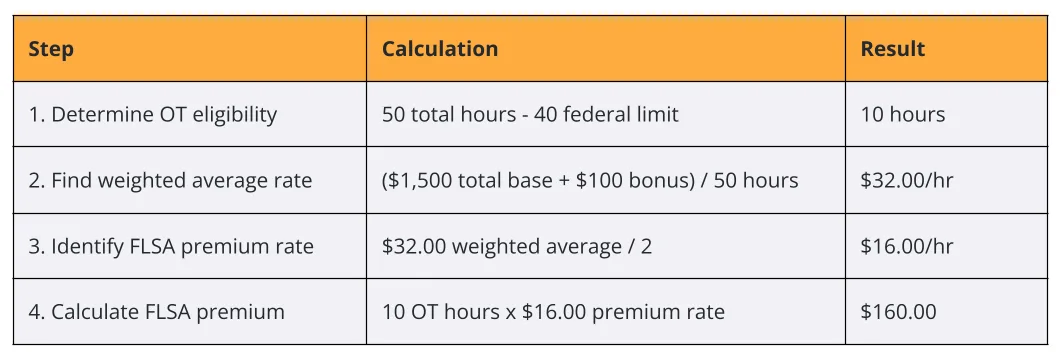

With both federal and state requirements in mind, here’s a step-by-step checklist for calculating federal overtime premium pay for each employee:

Determine overtime eligibility: Identify hours exceeding 40 per week or 80 per two-week period.

Find the weighted average pay rate: Divide total earnings by total hours worked.

Identify the FLSA premium rate: Divide the weighted average by two.

Calculate the FLSA premium: Multiply the premium rate by the number of hours exceeding 40.

Here’s what this calculation looks like in practice:

In one week, a field technician works 50 total hours. They have a base rate of $30 per hour, but because they worked on a specialized task for part of the week, their "weighted average" regular rate (including all earned differentials) is $32 per hour.

In this example, the amount you will track and report for Box 12, Code TT, is the $160.00 premium.

If your overworked accounting department is scrambling to do all of these calculations manually or relying on generic payroll software to stay compliant with the latest state and federal rules, they could be at risk of under- or overreporting QOC hours, which could trigger IRS inquiries or leave your construction firm liable for reporting errors.

According to the IRS penalty schedule, starting in 2026, failing to include the correct Code TT in Box 12 of the W-2 can result in standard IRS penalties of:

$60 per W-2 if corrected within 30 days.

$330 per W-2 if not corrected (capped at roughly $4 million per year for large businesses).

$660+ per W-2 if the IRS proves "intentional disregard."

These are stiff penalties on their own, but multiplied across tens, hundreds or thousands of employees, they can pose significant financial risk to your organization.

How Trimble can help

Fortunately, Trimble financial management solutions are built to handle the nuances of construction, including changes like the OBBBA. Here’s how Trimble can help you automatically identify and record qualified overtime hours directly from the field—saving your team time digging through old timesheets and outdated reports:

Automated FLSA calculations

Instead of calculating FLSA overtime premiums by hand, connected ERPs like Vista and Spectrum automatically aggregate hours and pay from weekly timecards to isolate the 0.5x premium amount required for the new OBBBA reporting. This ensures that even when your crews have multiple pay rates in a single week, your year-end data remains precise and audit-ready.

Construction-specific labor classifications

With Trimble financial management solutions, you can use specialized labor classifications for cash fringes, prevailing wage adjustments, etc. and include them in your final compensation numbers. This ensures you are not over-reporting or under-reporting the qualified premium on complex government or union jobs subject to prevailing wage rules.

Field-to-office connection

By connecting your field time-tracking directly to your back-office payroll workflows with field timesheet apps like Traqspera Field and Vista Field Management, you can be confident that when a worker enters their time on a jobsite today, your office is already prepared to report it correctly on a W-2 tomorrow—saving your team hours of manual work and ensuring you’re always audit-ready.

FAQ: What you and your crews need to know

Any changes to your field crew and project managers’ pay will almost certainly come with a few eyebrow raises and questions, especially as the tax season draws to a close. Here are a few FAQs that may come across your desk on what these tax updates mean for your workers.

Q: What does QOC mean?

Qualified overtime compensation (QOC) is the specific "half-time" premium pay required by Section 7 of the Fair Labor Standards Act (FLSA) that exceeds an employee’s regular hourly rate (the “half” in time-and-a-half pay).

Q: Does double-time pay count toward the deduction?

No. Only the "time-and-a-half" premium required by federal law is considered qualified.

Q: Is there a limit on how much employees can deduct?

Yes. The deduction is capped at $12,500 per year for individuals and $25,000 for joint filers.

Q: Which employees qualify for the overtime deduction?

The deduction applies only to hourly employees with a modified adjusted gross income of up to $150,000 for single filers and $300,000 for married couples filing jointly.