About this series:

We’ve all seen the headlines—the economy is currently a bit of a "fixer-upper" for contractors and owners. In times like these, an executive’s real job isn't just managing the day-to-day; it’s looking over the horizon to see what’s coming before it hits the job site.

To help you do just that, we’re thrilled to introduce our monthly series “Hard Hat Economics” with Dr. Anirban Basu. As the economist for the CFMA, ABC, AGC and AIA, Dr. Basu has an extraordinary ability to decode the indicators driving our industry. More importantly, he’s one of the few people who can make a deep dive into macroeconomic data, engaging and insightful. In the months to come, Dr. Basu will dive deep into complex economic shifts and what they mean specifically for you as a construction professional.

Why are we doing this? Because we believe that while you can't control the global economy, you can control how your business responds to it. Leading contractors don't just wait for a turnaround—they use these moments to sharpen their tools and modernize their operations.

Navigating a gloomy economy

The construction industry had a rough 2025. Industrywide employment declined by 4,000 positions, construction spending fell for just the third time in the past 15 years and materials price escalation—which had been nonexistent since the middle of 2022—reared its ugly, cost-boosting head.

The good news is that 2025 is over, and contractors entered the new year with plentiful optimism. As the saying goes, “hope springs eternal”.

The bad news is that the start of 2026 hasn’t been much better; the saying fails to mention that hope can be dashed just as easily as it springs, and there’s a real chance that industry optimism doesn’t survive the year’s first quarter.

Yes, construction employment levels bounced back in January, but that momentum was short-lived. Job losses resumed in February, with the industry shedding 11,000 net positions for the month.

While total construction spending in January was up 1% YOY from January 2025, it’s all but certain that nonresidential activity, buffeted by several headwinds, will continue to slow over the next few quarters.

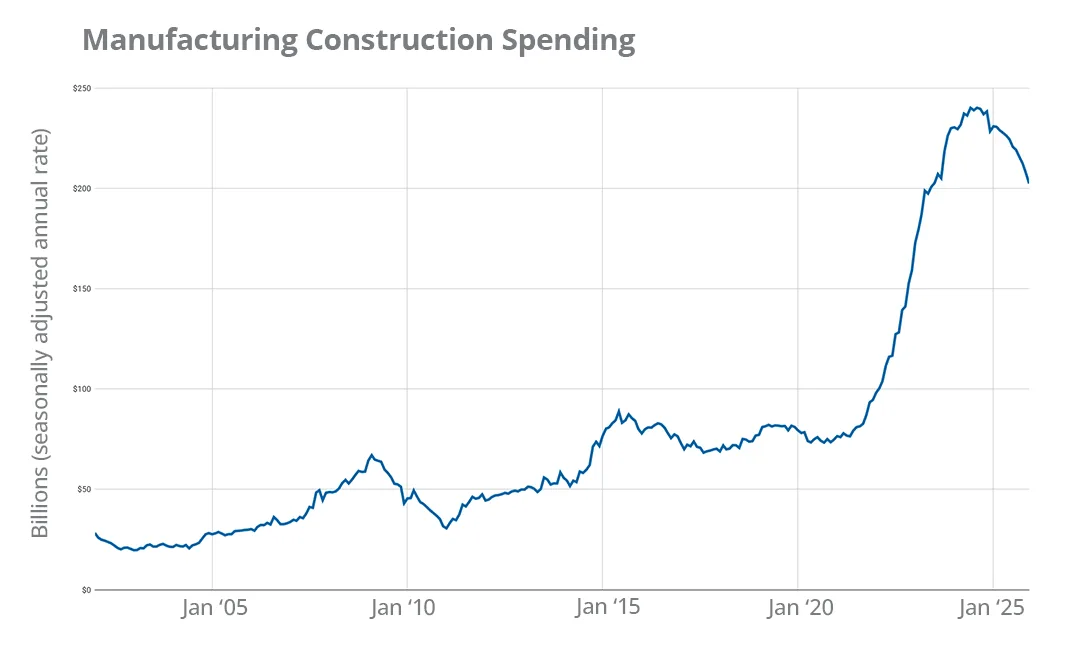

The most mechanical of those headwinds is the steadily unwinding manufacturing-related construction boom. Spending in the category rose meteorically in 2022 and 2023 due to the CHIPS Act, but those federally incentivized megaprojects are now wrapping up. As a result, manufacturing-related construction spending will drift slowly but surely back toward earth in 2026.

Manufacturing-related construction spending will likely decline in 2026. Chart source: U.S. Census Bureau.

Then there are stubbornly high borrowing costs. Despite three rate cuts during the second half of 2025, a skeptical bond market has prevented financing costs from falling. That has exacerbated the lingering effects of 2021 and 2022’s rapid materials price escalation, and there’s no way around it: construction services are expensive, and that’s suppressing activity.

Immigration policy has also put upward pressure on project costs by tightening the industry’s labor supply, even as construction spending contracts. Average hourly earnings for nonsupervisory construction workers were up 5.1% year over year in February, the largest annual increase in over two years.

The stiffest headwind remains the nearly unprecedented level of uncertainty caused by U.S. trade policy. While the recent Supreme Court ruling against the White House’s IEEPA tariffs has provided a smidgen of clarity, the tariffs on major construction inputs like iron and steel were imposed under a different law and remain firmly in place, while levies on other inputs remain in flux.

The conflict in Iran, which began at the end of February, has served as a gale-force intensifier to many of the aforementioned headwinds. Ten-year treasury yields have surged from sub-4% to approximately 4.3% at the time of this writing, putting further upward pressure on borrowing costs. While that’s unfortunate, it’s a minor consideration compared to the supply shock caused by the closure of the Strait of Hormuz.

Oil prices have exploded from about $60/barrel in late February to more than $90/barrel just a few weeks later. That will push construction inputs higher in two distinct ways. Directly, diesel is a major input to providing construction services, and its cost has surged from $3.80 per gallon two weeks ago to nearly $5.00 per gallon as of this writing. Indirectly, this will put upward pressure on shipping costs, and that will raise the cost of virtually every other input.

The lack of clarity regarding how long this conflict will last and how high oil prices might rise has exacerbated the already-damaging levels of economic uncertainty. At least in the short term, that could cause project owners to hold off on proceeding with large capital investments.

The bright side

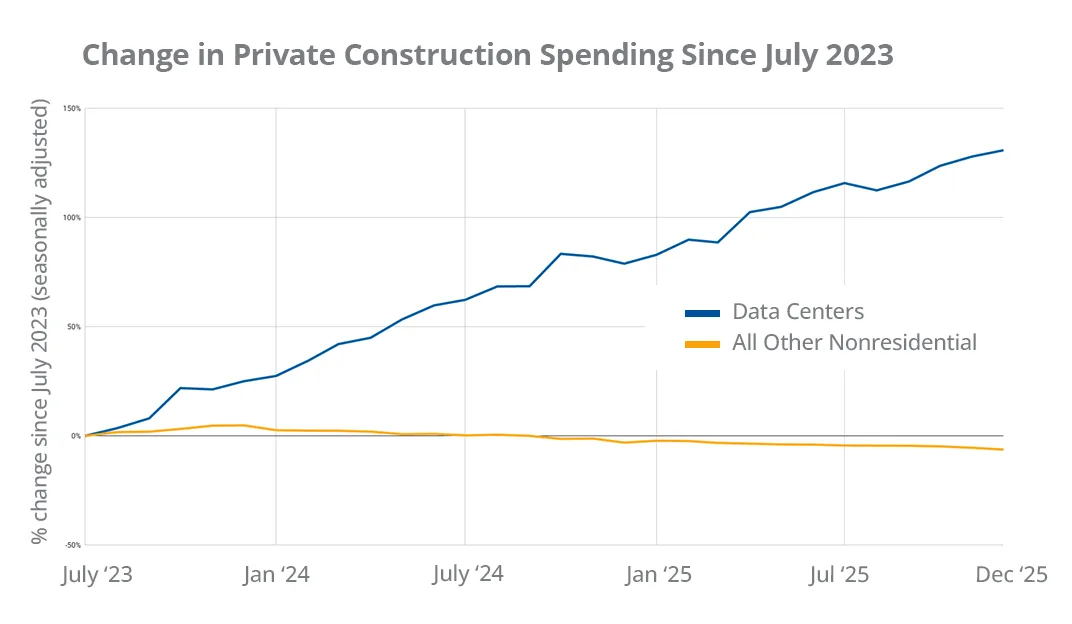

That’s what’s going wrong for the industry, but there are a few glimmers of light peeking through the gloom. The data center boom shows no signs of stopping, with activity in the segment up 131% over the past 2.5 years. That’s provided the industry with a critically important source of momentum; all other private nonresidential activity is down 6% over that span.

Data centers have provided critical momentum for the construction industries, while all other industries have slowed. Chart source: U.S. Census Bureau.

Of course, the benefits of that momentum have been relatively concentrated, with just 1 in 8 construction firms under contract to work on data center projects. Unsurprisingly, contractors that have data center work have nearly 50% longer backlog than those who do not, according to Associated Builders and Contractors’ (ABC) Construction Backlog Indicator.

Trade policy, for all the difficulties it’s caused, has likely spurred investment in certain manufacturing-related construction subcategories. Excluding the CHIPS-boosted computer/electronic subcategory, private construction spending on manufacturing structures rose a healthy 9% during 2025.

Contractors, for their part, remain confident about the year ahead. ABC’s Construction Confidence Index shows broad expectations of sales growth over the next six months, while the Associated General Contractors’ 2026 Construction Hiring and Business Outlook survey shows expectations of growth in most nonresidential segments.

The outlook

Despite recent challenges, the industry doesn’t need much to fall into place for activity to rebound. Lower borrowing costs would likely unleash pent-up demand, and that could lead to increased construction starts by late 2026 or the first few quarters of 2027. Of course, the same was true in early 2025. Over a year later, and the industry is still waiting for those lower borrowing costs.

Disclaimer:

The views and opinions expressed in this article are those of Dr. Anirban Basu and do not necessarily reflect the official policy or position of Trimble Inc. This content is provided for informational purposes only and should not be interpreted as financial, investment or economic guidance from Trimble.

Recording of last month’s economics webinar—how right was Dr. Basu in his predictions?

The only financial management platform built for small-business contractors. Streamline bidding, track real-time job costs and protect your profits.